Outgoing Nigeria’s President, Mr Muhammadu Buhari, has set booby traps for the incoming president, Mr Bola Tinubu, with critical last-minute economic decisions that could spell doom for the country after May 29 handover date.

Buhari has got the pliant Senate to approve his illegal N22.7 trillion Central Bank of Nigeria (CBN) ways and means securitisation fewer than four weeks to handover. With that, the N22.7 trillion owed the CBN will be turned into securities and sold as bonds.

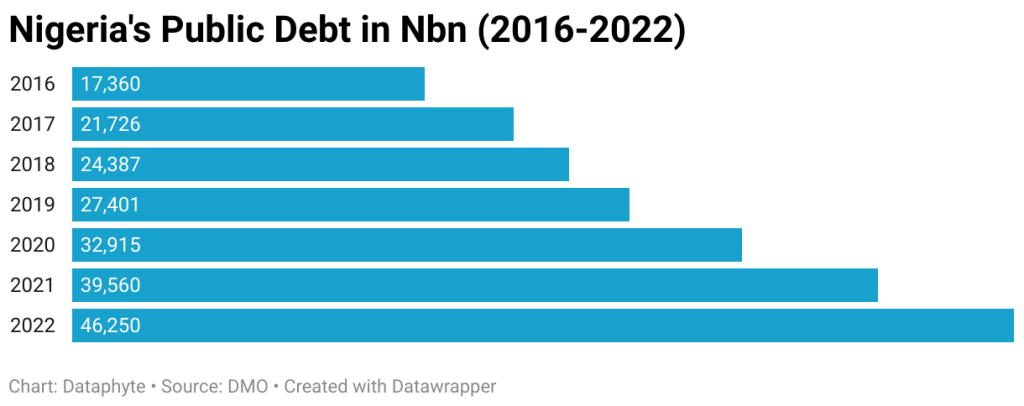

The retired general’s cap-in-hand disposition has raised public debt stock by 267 percent in eight years.

Buhari met public debt stock at N12.60 trillion in 2015 but has raised it to N46.25 trillion, which is 23.13 percent of the gross domestic product (GDP).

With the N22.7 trillion ways and means, Nigeria’s debt has hit N68.95 trillion, representing 58 percent of the GDP, which shows that the country under him does not produce enough output to pay its debt.

Little fiscal space

Buhari has left little room for the former Lagos State governor to borrow. A 2013 World Bank study, as reported by Kimberly Amadeo of Balance Money fame, said that if the debt-to-GDP ratio exceeded 77 percent for a long period, it would slow economic growth. In other words, Tinubu has only 19 percent band limit to borrow to meet immediate obligations facing him from May 29.

Tinubu will not have the same level of privilege accorded Buhari in terms of debt as any attempt to replicate his predecessor in this area will have immediate impact on the economy and consequently attract local and international condemnation.

Nigeria’s revenue-to-GDP ratio is nine percent, as against Ghana’s 13 per cent, Kenya’s 17 percent and Angola’s 21 percent. So, for Tinubu, borrowing in the short term may be inevitable, but he must now do so with tact, experts say.

Opportunities for revenue

However, Director-General of the Lagos Chamber of Commerce and Industry (LCCI), Dr Chinyere Almona, said in the light of the current revenue shortages, the new government should conduct an official identification of national utilities to determine their location, purpose and usage, and turn them into revenue-generating assets.

“There is, therefore, a need for government to take urgent steps to establish the market values of the assets, securitise the corporate assets and commercialise the real estate assets to raise revenue for the government and foreign exchange inflows for the country,” she advised.

She said there was also a need to replace existing debt stocks with asset-linked debt to reduce the debt servicing burden, while attracting greenfield Foreign Direct Investment (FDI) into publicly listed state-owned companies.

Second booby trap

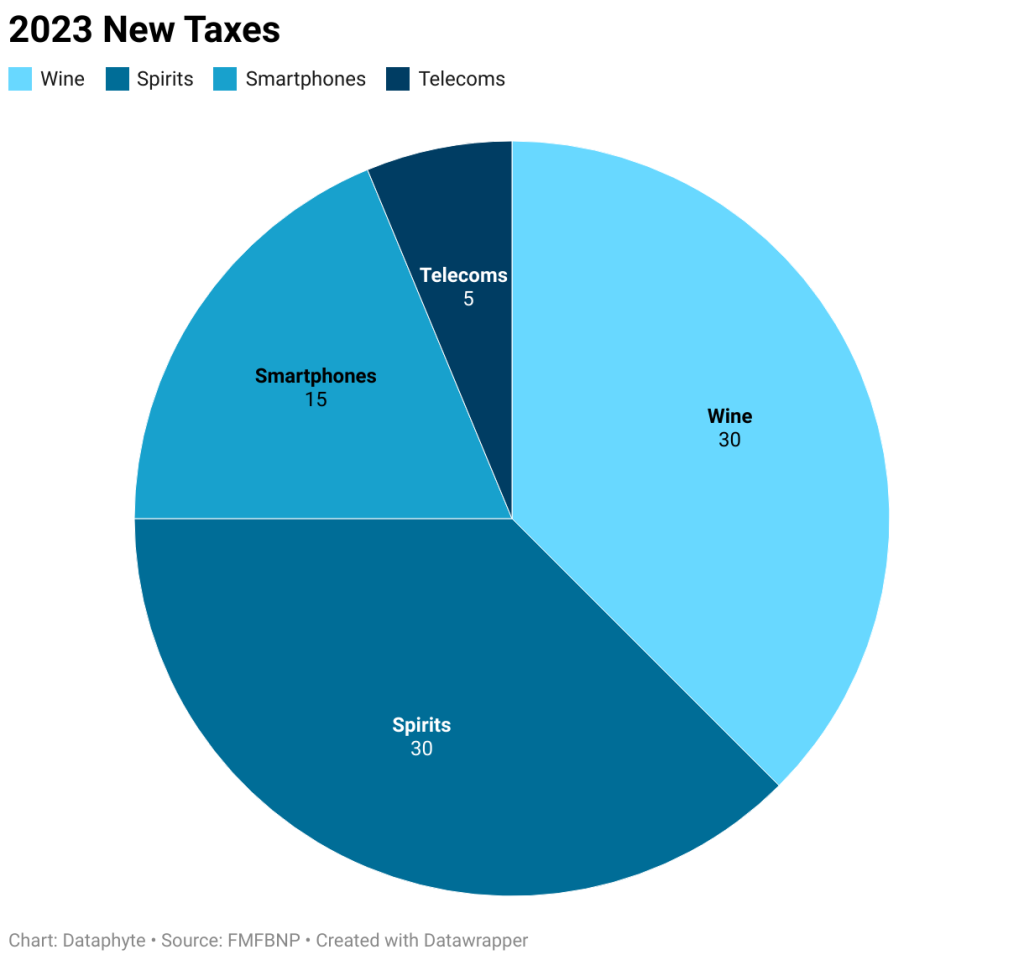

Another booby trap set by Buhari for Tinubu is a new tax regime, which the outgoing president might not have been able to implement. Buhari’s 2023 fiscal policy unveiled recently has imposed N10 per litre on non-alcoholic beverages, fruit juice, energy drinks. It has also imposed 20 percent ad valorem tax and N75/litre on beer and stout; 30 percent ad valorem tax and N75/litre on wine production as well as 30 percent ad valorem tax and N150/litre on spirit and other alcoholic beverages. Advalorem tax is measured on the basis of estimated value of goods. This is the second time Buhari is imposing taxes on beverages.

Buhari has also imposed 5 percent duty on telecoms services, and 15 percent tariff on smartphones (from 5-10 percent in 2022).

Tinubu must decide whether to retain these taxes or expunge them. Business owners argue that Nigeria is one of the countries with the highest level of corporate taxes in the world, with each company paying nearly 40 percent tax on profits annually.

Director-General of the Manufacturers Association of Nigeria, Mr Segun Ajayi-Kadir, told Dataphyte in a statement that this was worrisome and would kill off factories.

“It is worrisome that the current situation is indicative of inconsistency in Government policy, given that industries that are affected by excise tax administration, already made 3-year strategic plans based on the agreed calendar as scheduled in the roadmap including domestic and export sales prices, revenue and volume projections, tax burden calculations, etc. This in our opinion, may create credibility issues for the country with existing and potential investors, impacting Foreign Direct Investments (FDI) and the country’s Ease of Doing Business index among other implications,” he said.

Ajayi-Kadir said the taxes would lead to reduced production volumes with attendant result on downward trend in capacity utilisation, noting that the tax imposition would increase illicit trade in some of the affected products while eroding members’ market share and revenue, especially following continued devaluation of the naira against major currencies,

He noted that it would squeeze manufacturers’ margins and force them to pass additional costs to consumers by way of higher prices.

Director-General of Centre for the Promotion of Private Enterprise, Dr Muda Yusuf, said the new taxes would lead to loss of direct and indirect jobs and hurt investments.

“Sustaining current investments in these sectors would be a herculean task. These policy measures failed to reckon with the multifarious challenges

which industry operators are currently grappling with,” he said.

Bigger trap

Moreover, Buhari has refused to honour his words by removing petrol subsidies which have gulped trillions of naira in his eight-year reign. He passed the buck to the next administration by projecting to root out the opaque regime by June. Experts believe he was trying to be clever by half, knowing he would be in Daura by June 2023.

Buhari has set Tinubu up. Should Tinubu remove the subsidies, he will have labour unions (who did not support his emergence and could ruin him) and galloping inflation to contend with. Should he retain the subsidies, he will have fewer resources to execute his plans. .webp)

Subsidy payments have risen from N240 billion in 2016 to over N1.5 trillion in the half-year, 2022. This year, Buhari will spend N3.36 trillion on petrol subsidies in the first six months. This could reach N6.7 trillion by December 2023 should Tinubu choose to retain them.

“I do not envy Tinubu,” said an emerging markets analyst, Mr Ike Ibeabuchi. “His hands have been tied by Buhari on many fronts. I wish him good luck,” he quipped.

But he advised the incoming presodent to phase subsidy removal to avoid protests and social tensions, noting that he must cut the cost of governance in order to have sufficient resources to execute his vision.