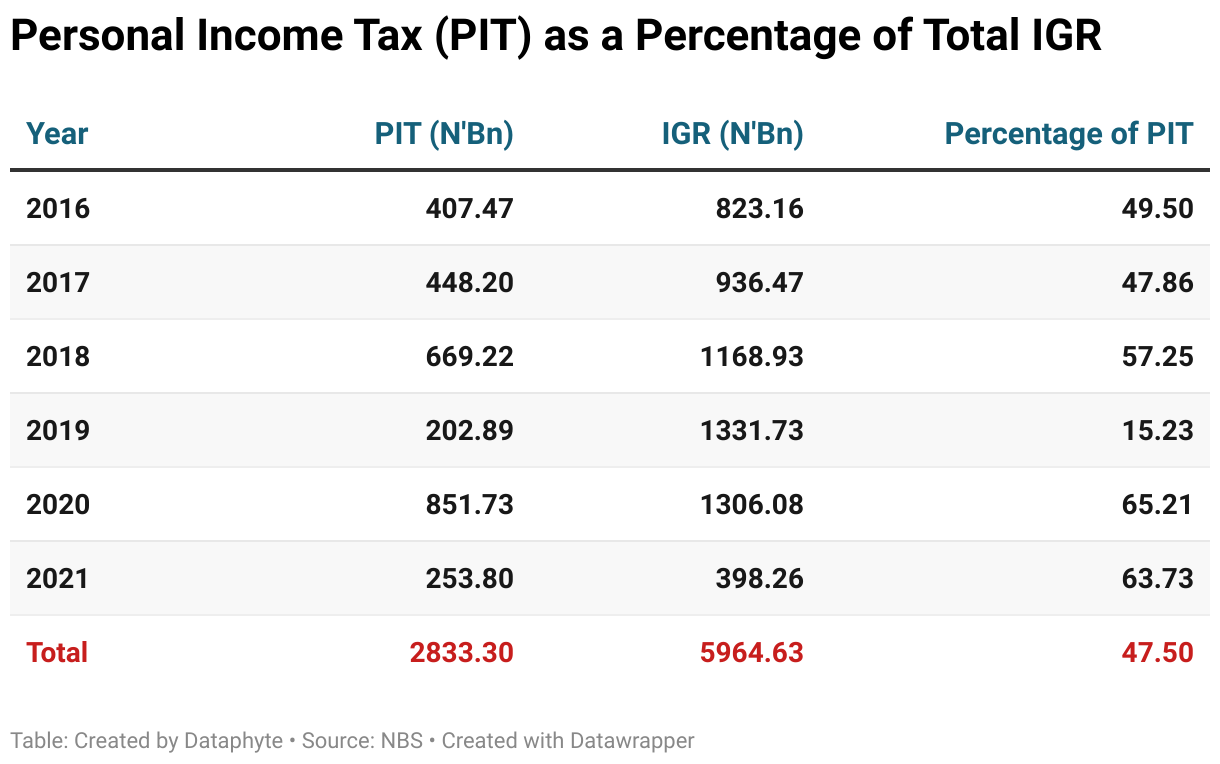

Personal Income Tax (PIT) or residency tax remains the primary source of income for state governments. This source forms most of the state governments’ revenue annually. In five and a half years (2016 to half-year 2021), out of the N5.964 trillion generated, PIT summed up to N2.833 trillion, making up 47.5% of the figure.

Residence tax has always contributed substantially to the total IGR of states and FCT within the last five years except in 2019. The highest of this proportion was recorded in 2020, where it accounted for 65.2% of the total IGR. Total IRG in 2020 was N1.31 trillion, out of which PIT summed up to N851.73 billion.

In 2016, 49.5% of the total IGR was PIT. The proportion of the preceding years shows that 2017 had 47.9%, 2018 57.3%, 2019 15.2%, and the half-year proportion in 2021 is 63.7%.

This substantial figure of PIT to IGR has generated age-long controversies between states whose workers reside within their territory but work in other neighboring states. These states see a considerable amount of their potential PIT revenue taken by other states.

This is the case with states like Ogun, Nasarawa, Niger, and Kogi, whose citizens/residents often work in Lagos and the Federal Capital Territory (FCT).

The Lagos state government agreed to remit 20% of the PIT generated by the state on workers residing in Ogun state to the Ogun state government. However, in the case of Nasarawa state for its residents working in the FCT, the government insists on 100% remittance of PIT on workers residing in its state.

Residence tax is paid in Nigeria for an individual who has resided in any part of the country for a minimum period of 183 days in any 12 months. Thus, people living in one state and working in another make the situation dicey as they can be adjudged to spend 183 days in either state based on the hours spent.

The issue of residency remains crucial to income tax generation, not only in Nigeria but around the globe. In the United States, this problem arises with states collecting income tax from citizens whose residence transcends one state. To clarify, the state uses some factors to define residency irrespective of the 183 days spent in a state. Among these factors are employment location, employment classification (permanent or temporal), and location of business relationship and transaction.

In Europe, there is a fictitious tax residence to address this. Under this, an individual is liable to pay their income tax in a place where they earn all or most of their income even though not residing there. Thus residence tax is collected based on the location of income source rather than where one lives.

Here in Nigeria, the Personal Income Tax Act of 2011 defines the principal residence as the location of the branch or operational site where an individual works, provided there is a minimum of 50 workers there.

This explicitly explains why Lagos and the FCT should continue to collect the residence tax of workers within their territory even though they reside in other neighboring states.

The Lagos state government’s decision to remit 20% of the residence tax collected on the income of residents from Ogun state is simply an act of benevolence to Ogun state. Furthermore, putting the Personal Income Tax Act into perspective, Nasarawa state does not have the legal basis to demand any portion of PIT collected by the FCT on residents’ income in its state working within the FCT.

However, these states can improve their residence tax pool by attracting investments to their states. This they can do through conscious infrastructural development and creating an enabling environment where businesses can thrive. This will increase the number of employed citizens residing within their states, thus increasing residence tax.